|

|

||||||||

|

||||||||

A Look Into the Markets |

This past week, interest rates continued to hover near three-year lows headed into the Fed Meeting. Let's talk about what happened, the impact, some positive housing news and what to watch in the week ahead. "California sunlight, sweet Calcutta rain, Honolulu starbright, ooh-ooh-oh." The Song Remains the Same, Led Zeppelin. The Fed Meeting Last week's Fed meeting came and went largely as expected, with no change to policy. What did matter was the language. The Fed upgraded its assessment of economic growth, describing activity as expanding at a "solid" pace, compared to "moderate" in prior statements. That subtle shift reinforces the Fed's current stance: the economy is holding together well enough that there is no urgency to cut rates. "I'd say that the upside again, the upside risks to inflation and the downside risks to employment have diminished." Fed Chair Jerome Powell, January 28, 2026. This quote from Mr. Powell's press conference was likely the most important statement he made, as it highlights a lower risk of higher inflation and higher unemployment. There were two notable dissenters. Governors Stephen Miran and Christopher Waller both voted for a 25-basis point cut, signaling that while the committee is comfortable waiting, there is still an internal debate about when to cut rates again. Chair Powell avoided political questions entirely during the press conference and consistently steered the message back to the economy and monetary policy. He also said the Fed believes the economy is in an "OK" place and that it can afford to be patient as it waits for additional inflation and labor market clarity. The markets seemed to agree as stocks moved higher and mortgage rates moved lower after the Fed Meeting concluded. Housing Price Gains Ease On the housing front, the S&P Case-Shiller Home Price Index for November rose 1.4% year-over-year. This is welcome news. A slower pace of home prices coupled with lower mortgage rates would help with affordability. Looking ahead, 2026 is expected to be the first time in 15 years that wage growth outpaces home price appreciation. That doesn't fix affordability overnight, but it will be a continued step in the right direction. 4.20% From a rates perspective, the 10-year Treasury yield popped back above 4.20%, a level that acted as a ceiling for much of last year and continues to be a key line in the sand. If the 10-year stays north of 4.20%, mortgage rates are unlikely to see meaningful improvement. Sustained progress lower in mortgage rates will require the 10-year to decisively break beneath that level. 30-yr Mortgage Rates and 10-yr Note 30-Year Fixed Mortgage Rates (Freddie Mac daily average, January 29, 2026)

10-Year Treasury Note Yields (daily close, January 29, 2026)

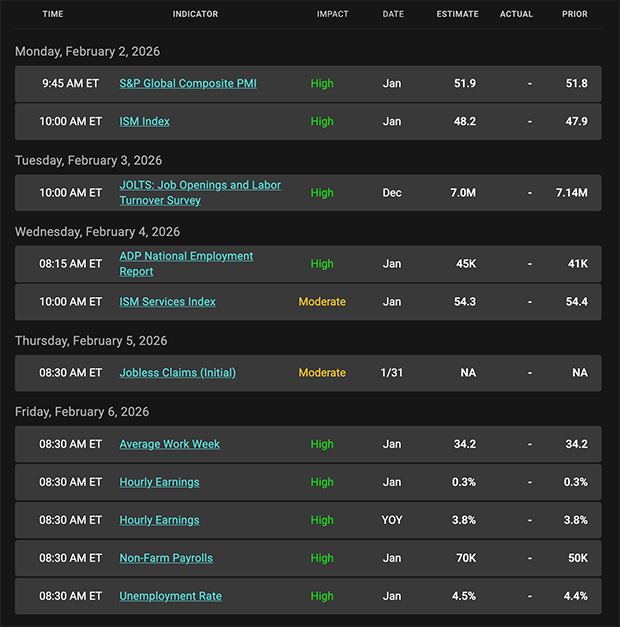

Looking Ahead Next week's attention is centered on the labor market. We'll be watching ADP employment, JOLTS, and the Jobs Report for confirmation that the labor market continues to cool gradually. There are no notable Treasury auctions scheduled. Fed speak resumes with the Fed Meeting now in the rearview mirror. As always, stay focused on managing expectations. The rate environment remains range bound, but the longer-term affordability story is slowly improving. |

Mortgage Market Guide Candlestick Chart |

|

Each candle represents one day of trading. As mortgage bond prices move higher, rates move lower. You can see on the right side of the chart, how mortgage bond prices continue to trade within a whisker of three-year highs, meaning three-year rate lows. Chart: Fannie Mae 30-Year 5.0% Coupon (Friday, January 30, 2026) Economic Calendar for the Week of February 2 - 6 |