|

|

||||||||

|

||||||||

A Look Into the Markets |

This past week, interest rates hovered near the lows of 2026 and close to the best levels we've seen over the past three years, driven largely by headlines surrounding the next potential Federal Reserve Chair. Let's break down what happened, and what lies ahead in a critical week for markets. "Pick up my guitar and play Just like yesterday Then I'll get on my knees and pray Kevin Warsh Tapped as Next Fed Chair The biggest story shaping rate expectations wasn't an economic report; it was President Trump signaling Kevin Warsh as his choice to succeed Jerome Powell when Powell's term ends in May. Markets are already starting to price in what a Warsh-led Federal Reserve could mean for the economy and interest rates. First, a reminder: the Fed does not control mortgage rates. Mortgage rates are driven by the bond market, inflation expectations, and economic growth. What the Fed does control is policy; how aggressively it fights inflation, how it views economic growth, and how it balances maximum employment. Those decisions influence bond yields, which is where mortgage rates ultimately live. Warsh represents a meaningful philosophical departure from the modern Fed. After leaving the Fed in 2011, he became openly critical of quantitative easing and has made it clear he does not support the Fed buying Treasuries or mortgage-backed securities. He has also argued for shrinking the Fed's balance sheet while lowering the Fed Funds rate, with the goal of helping Main Street and small businesses rather than supporting financial assets. Perhaps most notably, Warsh believes strong economic growth and even an economy running "hot" is not inherently inflationary. That's a sharp contrast to the Fed's posture over the past decade. We'll soon learn more as he begins speaking publicly, but markets are already paying attention. Economy Remains Resilient Complicating the picture for the Fed, the economy appears to be reaccelerating. GDP growth over the past two quarters has come in north of 4.00%, and the most recent ISM Manufacturing PMI delivered its first expansion reading since January 2025. Susan Spence, MBA, Chair of the Institute for Supply Management, summarized it well: "In January, U.S. manufacturing activity returned to expansion territory, with improvements across all five PMI subindexes. This is welcome news for the economy." For the Fed, however, stronger data adds a "wait-and-see" element before cutting rates. Government Shutdown Was Transitory A brief government shutdown limited several data releases, and Friday's Jobs Report was postponed despite the government reopening midweek. The lack of fresh data left the 10-year Treasury note stubbornly above 4.20%; a level it has failed to break below for weeks, continues to cap meaningful improvement in mortgage rates. Rate Cut Futures: Why a Coin Toss? So why are CME Fed Funds futures pricing the next rate cut for June, and only as a coin flip? Markets are caught between two opposing forces: improving growth data that argues against cuts, and the possibility of a future policy shift at the Fed that could eventually allow them. Until inflation data provides clarity, conviction remains limited. 30-Year Mortgage Rates and 10-Year Note 30-Year Fixed Mortgage Rate (Freddie Mac daily average, February 5, 2026)

10-Year Treasury Note Yield (daily close, February 5, 2026)

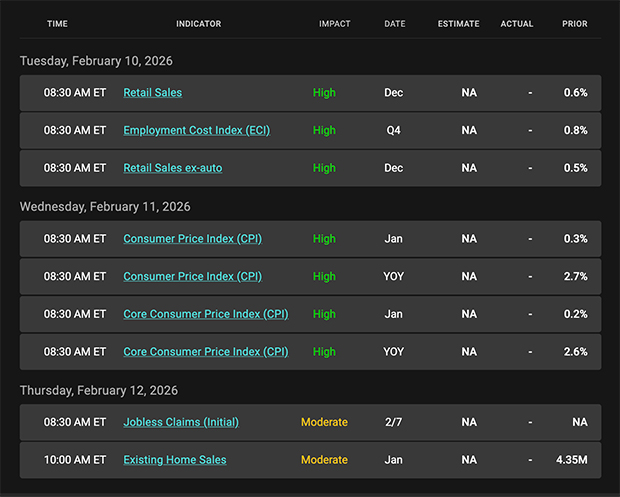

Looking Ahead Next week is a big one. The January Jobs Report will be released on Wednesday the 11th while January CPI and Retail Sales headline the economic calendar and will be critical inputs for rate expectations. Adding to potential volatility is a heavy slate of Treasury auctions, including the 10-year note and 30-year bond. How these auctions are received will offer important insight into investor demand at current yield levels. Strong demand could help limit upward pressure on rates while weak demand would suggest the opposite. |

Mortgage Market Guide Candlestick Chart |

|

Each candle represents one day of trading. As mortgage bond prices move higher, rates move lower. On the right side of the chart, mortgage bond prices continue to trade near three-year highs, translating to three-year lows in mortgage rates. Chart: Fannie Mae 30-Year 5.0% Coupon (Friday, February 6, 2026) Economic Calendar for the Week of February 9 - 13 |