|

|

||||||||

|

||||||||

A Look Into the Markets |

Mortgage rates pushed up to fresh 2026 highs this week as global bond markets remained under pressure. Let’s break down what happened, why rates moved higher again, and what to watch in the week ahead. “So put me on a highway. And show me a sign. And take it to the limit one more time.” - Take It to the Limit, The Eagles Iran Conflict Unresolved The market continues to wrestle with uncertainty surrounding the Iran conflict, and right now there is still no clear resolution in sight. Investors were hoping for signs of de-escalation, but ongoing tensions in the region continue to keep energy markets on edge. Oil prices are now hovering near the $100 per barrel level, and that matters for mortgage rates. Historically, oil prices and long-term interest rates tend to ebb and flow together because higher energy costs feed inflation fears throughout the economy. When oil spikes, investors worry inflation could remain stubbornly elevated, which pressures bond markets and pushes yields higher. That is one of the key reasons why 30-year mortgage rates moved to the highest levels of the year this week. Elevated oil prices are making it difficult for rates to move meaningfully lower. Global Inflation Fears This is not just a U.S. story. Global bond yields are climbing sharply as investors worry about inflation, growing government debt loads, and rising deficits around the world. In Japan, the 10-year government bond yield recently climbed to the highest level since 1996, while Japan’s 30-year bond yield pushed to record highs. In the UK, 30-year gilt yields surged to the highest levels since 1998. Germany’s 30-year bond yield has climbed to the highest level since 2011. The common theme globally is concern that governments will need to continue issuing massive amounts of debt at a time when inflation risks remain elevated. That combination is keeping upward pressure on rates worldwide, including here in the U.S. Housing Starts and Permits Housing Starts showed residential construction activity fell 2.8% in April to a seasonally adjusted annual rate of 1.465 million units. While activity declined from March levels, the number still came in better than expectations of 1.420 million and was 4.6% higher than one year ago. Single-family starts fell 9.0% from the previous month and were down 2.4% year-over-year, highlighting ongoing affordability pressure tied to elevated mortgage rates. However, multi-family construction remained stronger, rising 14.3% from March and up 23.3% versus last year. The bigger takeaway is that housing data remains volatile month-to-month, which is why longer-term trends matter more than any single report. Builders continue to navigate higher financing costs, affordability challenges, and uncertain buyer demand, but this report did show some resilience in overall construction activity despite rates remaining elevated. Building permits, which often provide insight into future construction activity, also continue to suggest builders remain cautious but active as they balance supply needs against affordability headwinds. 4.60% The 10-year Treasury Note is once again trading near the highs of the year and around an important technical level near 4.60%. Going back over the past several years, every time yields climbed above the 4.60% area, rates were lower three months later. That does not guarantee history repeats itself this time, especially with ongoing uncertainty surrounding Iran and oil prices, but technically speaking, the longer a ceiling like 4.60% exists, the more formidable it becomes. Markets are clearly testing that level right now. 30-Year Mortgage Rates and 10-Year Note 30-Year Fixed Mortgage Rate (Freddie Mac daily average, May 21, 2026)

10-Year Treasury Note Yield (daily close, May 21, 2026)

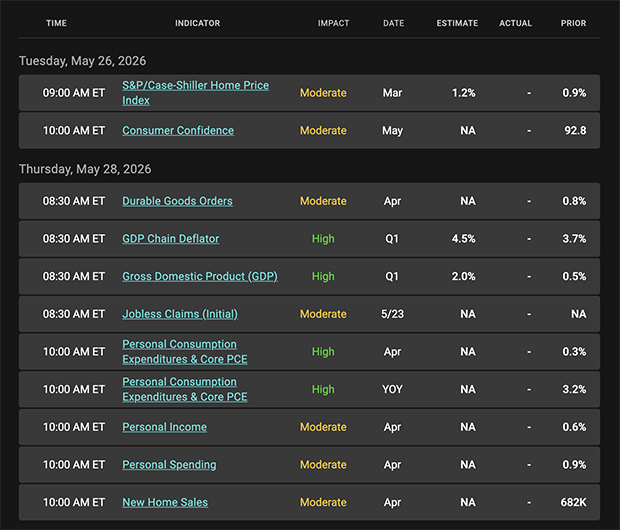

Looking Ahead Next week brings several important economic reports and Treasury auctions that could impact mortgage rates. On the economic side, markets will focus on: Consumer Confidence, the second read on Q1 GDP, Core PCE Inflation. We will also see Treasury auctions for: 2, 5 and 7-year Notes. The auction demand will be closely watched given the recent rise in global yields. Additionally, this will be Fed Chair Kevin Warsh’s first full week on the job, and markets will be paying close attention to both his tone and any signals regarding inflation, rates, and future Fed policy. Right now, elevated inflation concerns and rising global yields continue to keep pressure on mortgage rates. As always, we will continue watching the bond market closely and keeping you updated throughout the week. |

Mortgage Market Guide Candlestick Chart |

|

Each candle represents one day of trading. As mortgage bonds prices move higher, rates move lower. You can see on the right side of the chart, how mortgage bond prices drifted lower to the worst levels of 2026. Chart: Fannie Mae 30-Year 5.5% Coupon (Friday, May 22, 2026) Economic Calendar for the Week of May 25 - 29 |