|

|

||||||||

|

||||||||

A Look Into the Markets |

“The waiting is the hardest part. Every day you see one more card. You take it on faith, you take it to the heart. The waiting is the hardest part” - The Waiting by Tom Petty. Interest rates held relatively steady this past week as markets prepare for Kevin Warsh's first Federal Reserve meeting as Fed Chair. While investors continue to digest economic data and geopolitical developments, the bond market appears content to remain in a holding pattern until it receives additional guidance from the Fed. Let's take a look at what happened this week and what could be a very important week ahead for rates. Iran Conflict Ongoing The largest headwind facing both the overall economy and interest rates remains the ongoing conflict involving Iran and the resulting impact on energy prices. Oil prices remain elevated compared to levels seen earlier this year, and that has created upward pressure on inflation expectations. The good news is that energy markets have remained orderly despite the uncertainty, and investors continue to hope for a de-escalation that could allow oil prices to move lower. However, meaningful mortgage rate improvement may remain limited until energy prices retreat further. Historically, oil prices and 30-year mortgage rates tend to ebb and flow together, making energy costs one of the key variables for the rate outlook moving forward. CPI Hits Multi-Year High, But... This week's Consumer Price Index (CPI) report showed headline inflation rising to its highest level in several years, driven largely by the recent surge in energy prices. The increase serves as a reminder that inflation pressures can quickly reappear when commodity prices move sharply higher. At the same time, there was encouraging news beneath the surface. Core CPI, which excludes food and energy, increased just 0.2% for the month. That reading came in below expectations and was welcomed by the bond market. While headline inflation grabbed the headlines, the softer Core CPI figure suggests that underlying inflation pressures remain more contained than many feared. The Cure for Higher Rates One of the most encouraging developments this past week came from the Treasury market. The government auctioned a significant amount of debt, and investor demand remained solid throughout the process. Strong Treasury auction demand signals that investors continue to view current yields as attractive and are willing buyers at these levels. This matters because sustained investor demand can help place a ceiling on long-term interest rates. There is an interesting trend developing that dates back more than 15 years. Every time the 10-year Treasury Note has moved above 4.60%, it has failed to remain there three months later. Earlier this spring, the 10-year yield touched 4.69%, challenging that historical ceiling once again. Now the clock is ticking. The longer rates remain unable to establish themselves above 4.60%, the greater the possibility that this long-standing trend remains intact. While no indicator is perfect, history suggests that sustained moves higher in rates become increasingly difficult once the 10-year reaches these levels, supporting the view that we may be witnessing the upper end of this rate cycle. 30-Year Mortgage Rates and 10-Year Note 30-Year Fixed Mortgage Rate (Freddie Mac daily average, June 11, 2026)

10-Year Treasury Note Yield (daily close, June 11, 2026)

Looking Ahead There are several economic reports on the calendar that could influence trading in the week ahead, but the main event will undoubtedly be the June Federal Reserve meeting; the first under new Fed Chair Kevin Warsh. Markets will be listening carefully not only for policy decisions but also for clues regarding potential changes to how the Federal Reserve communicates with investors. Warsh has previously expressed interest in reducing the Fed's reliance on forward guidance and limiting the amount of ongoing Fed commentary that influences markets. Investors will also be watching for discussion surrounding Quantitative Tightening (QT), which remains one of the Fed's primary tools for extinguishing inflation pressures. In addition, there could be changes to the Summary of Economic Projections (SEP), a report that has become a major driver of market expectations over the years. Whether these changes arrive immediately or are simply discussed as future possibilities, this meeting could provide important insight into how the Fed operates under its new leadership. As always, we'll be watching closely and keeping you informed every step of the way. |

Mortgage Market Guide Candlestick Chart |

|

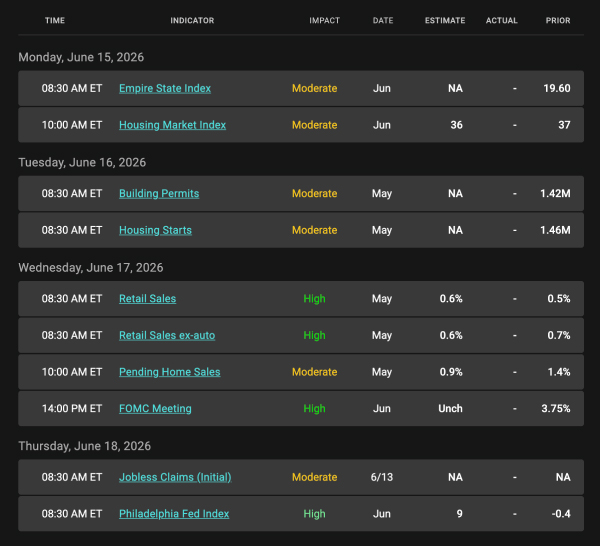

Each candle represents one day of trading. As mortgage bonds prices move higher, rates move lower. You can see on the right side of the chart, how mortgage bond prices hover just above the price lows of 2026, meaning the rate highs of 2026. Chart: Fannie Mae 30-Year 5.5% Coupon (Friday, June 12, 2026) Economic Calendar for the Week of June 15 - 19 |